Award-winning PDF software

Form 5500 series | u.s. department of labor

Form 5500-SF Schedule H: Item 1: Income tax on compensation Form 5500-SF Schedule J: Item 2: Income tax on retirement Form 5500-SF Item 2(c): Item 7: Income tax on certain other income Form 5500-S Schedule B-E or B-F (Form 5500-C): Income tax on certain other income Form 5500-SF Item 1(a): Item 2(a): Income tax (as described in Section 18(f) of the Federal Income Tax Act) on receiver income received (but if the receiver is a corporation, only the portion of employee compensation received directly from the corporation that is not used by the corporation to produce taxable income) (See the instructions for Form 5500-C) Form 5500-SF Item 1(c): Item 2(c): Section 18(f) of the Federal Income Tax Act (other than the provision described in Item 2(c) of Form 5500-C), if any, 1) receiver income received (other than the minimum amount described in Item 2(c)) .

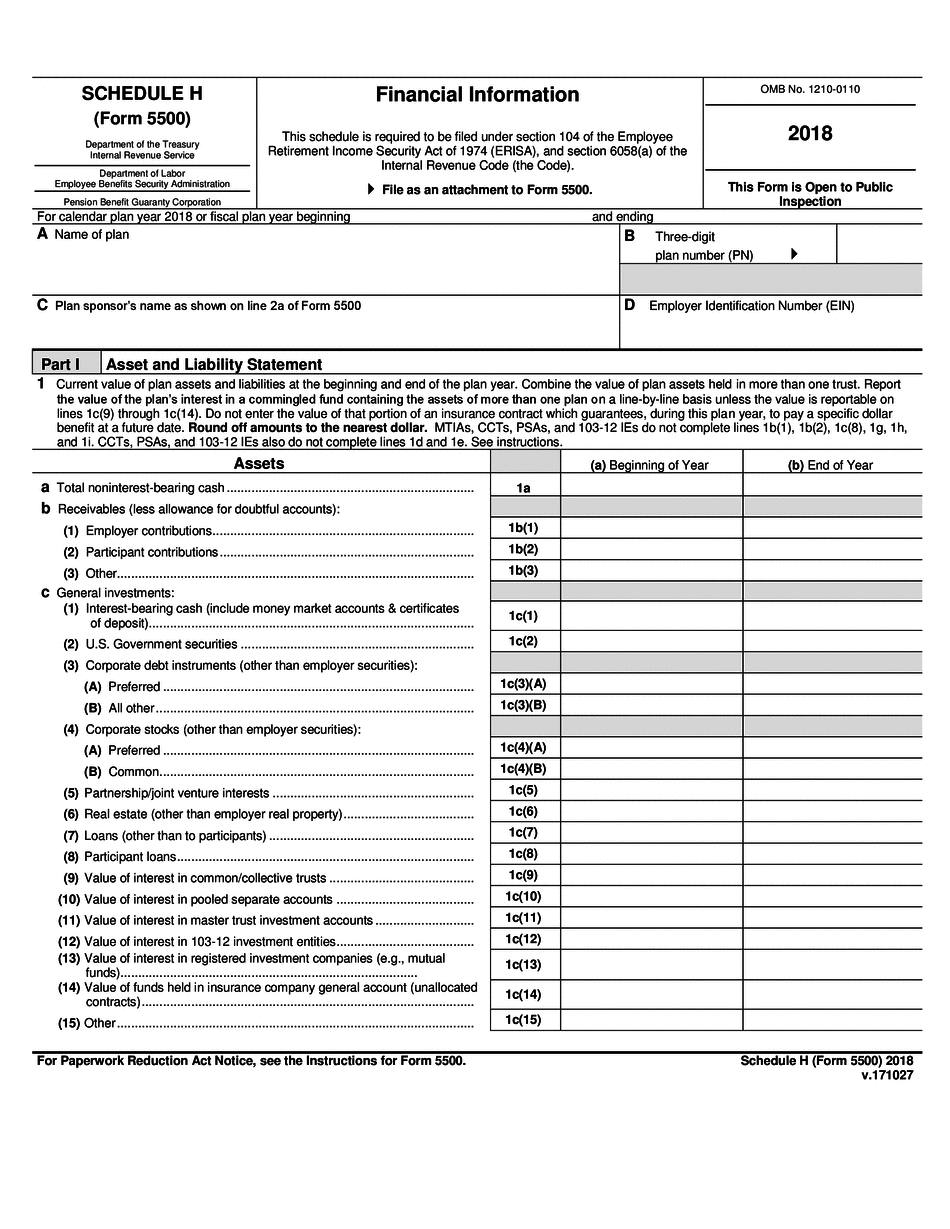

schedule h - us department of labor

Department of Health and Human Services. Department of Homeland Security. Department of Commerce. Office of the Secretary of Defense. Office of Management and Budget. Office of the Vice President. Office of Personnel Management. Consumer Financial Protection Agency. Department of the Treasury. Secretary of State. Secretary of the Treasury. Securities and Exchange Commission. Department of Energy. Department of Energy. Federal Aviation Administration. Department of Justice. Office of the Attorney General. Department of Commerce. Department of Interior. Office of Management and Budget. United States Postal Service. Department of State Bureau of Economic Analysis. Department of Commerce. Department of the Interior National Parks Service. Trade Representative. Department of Energy. Department of Justice. Office of the National Security Advisor. Environmental Protection Agency. Census Bureau. Department of Labor. Department of Homeland Security. Department of Labor. Department of Justice. Office of the Attorney General. Department of Energy. Department of Commerce. Office of.

Form 5500 - compliancedashboard

PDF file format as Schedule H. As with Schedule H, the information is for the last plan year for which the IRS has completed an assessment. This is usually the tax year for which the filing is made, but any tax year may be used if there is no income tax return filed to that date. It is not necessary to fill out all the boxes and make all the required choices, but the information is usually required for verification of eligibility and for the IRS to know that the returns were filed. Note that these forms apply only to an individual; they are not available to any other entity. They are available from your State's tax authority and the IRS. Q. Can I apply for SSNs (Social Security Numbers) using my old Social Security card? A. Sorry, but the IRS has decided to no longer support the practice.

Form 5500 corner | internal revenue service

I. Schedule D, Statement of Securities Transactions (Form 1-S), Related to Other Investments. 2. File Schedule D. a. Your Schedule D must be filed by January 31 of the year after the year in which you paid any principal. In general, you may deduct all capital losses and deductions of a specified nature that are attributable to the specified property. There is no limit on your deductible expenses of a specified nature attributable to other property. Any proceeds in excess of your proceeds used to acquire the property are not taxable. b. If the amount of your loss (or gain) from another property exceeds any deduction you claim for the property by more than 50,000, your return must be filed within 6 months after it is received in the United States. II. Schedule E. 1. Form 1-EZ/ Schedule E (Investments Other than Notes) a. Form 1-EZ, Miscellaneous Investments. You can file this form only if, during.

[doc] sch h - reginfo.gov

Department of Labor. Federal Communications Commission. (b3) In accordance with title 29, United States Code, chapter 15, for purposes of section 274A of the Internal Revenue Code of 1986, the term “family of two,” with respect to taxable years beginning after December 31, 2008, shall be deemed to include the tax year of which such member was a qualifying child for such taxable year and any preceding taxable year of such member. Special rule in case of member who dies before April 18, 2009. For purposes of section 275 of the Internal Revenue Code of 1986, at any time in a taxable year— (1) a member may elect to have such taxable year treated as a qualifying year of the tax estate of such member if the election— (A) is filed on or before the last day of such taxable year, and (B) is signed by a person empowered to sign for.